How good is the Aussie economy? On the back of the stable outlook on our AAA sovereign credit rating, last week’s employment data showed a better-than-expected post-COVID recovery in terms of the headline unemployment rate and overall workforce participation. This has led to speculation of a potential uplift in wages, due to labour shortages amplified by the current halt on immigration (thanks to closed borders).

But where will this expected wage growth actually come from?

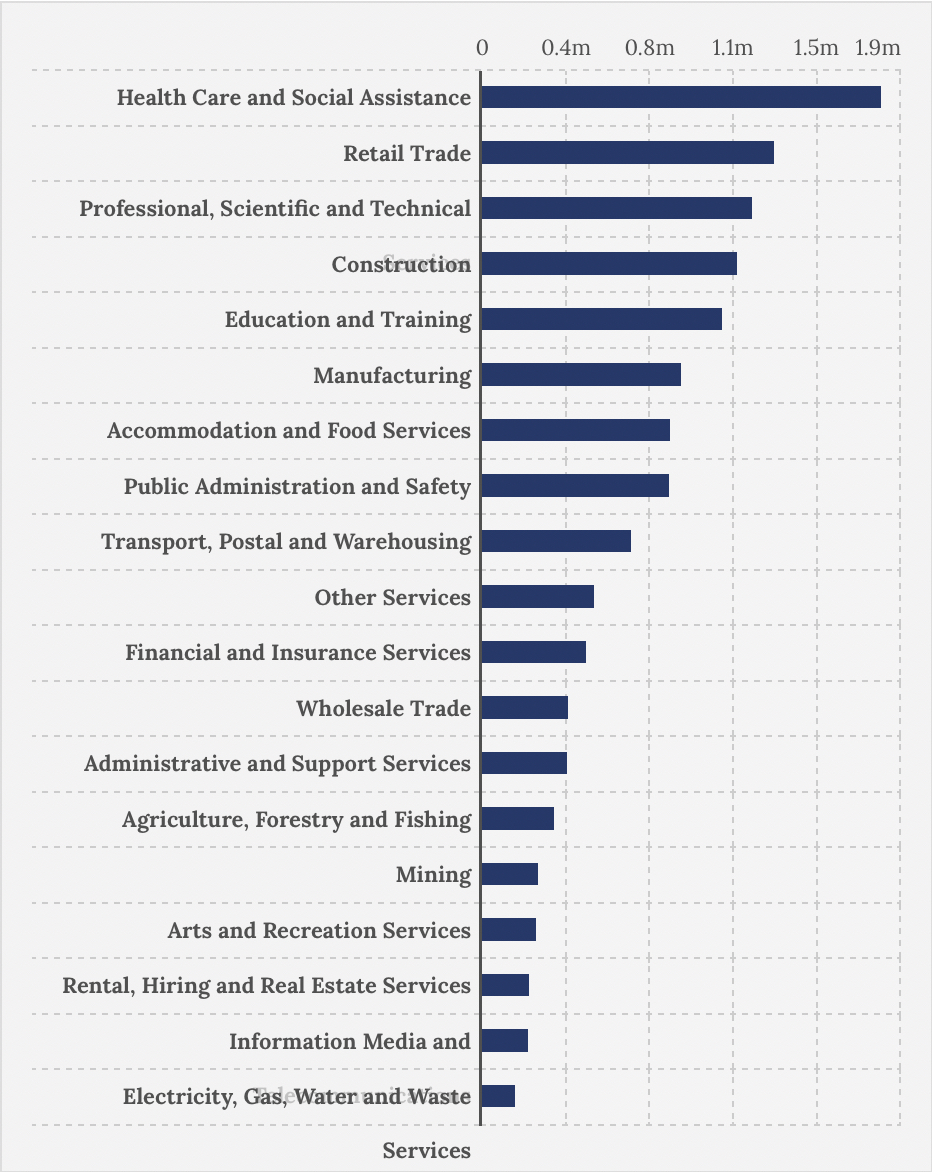

According to ABS data for February 2021, the top 5 industries by number of people employed are: Health Care; Retail Trade; Professional, Scientific and Technical; Construction; and Education. (See above chart.)

Now, contrast this with three other relevant data points: 1) the number of Australian companies by size; 2) the annual change in employment growth/reduction by industry; and 3) the national GDP contribution by industry.

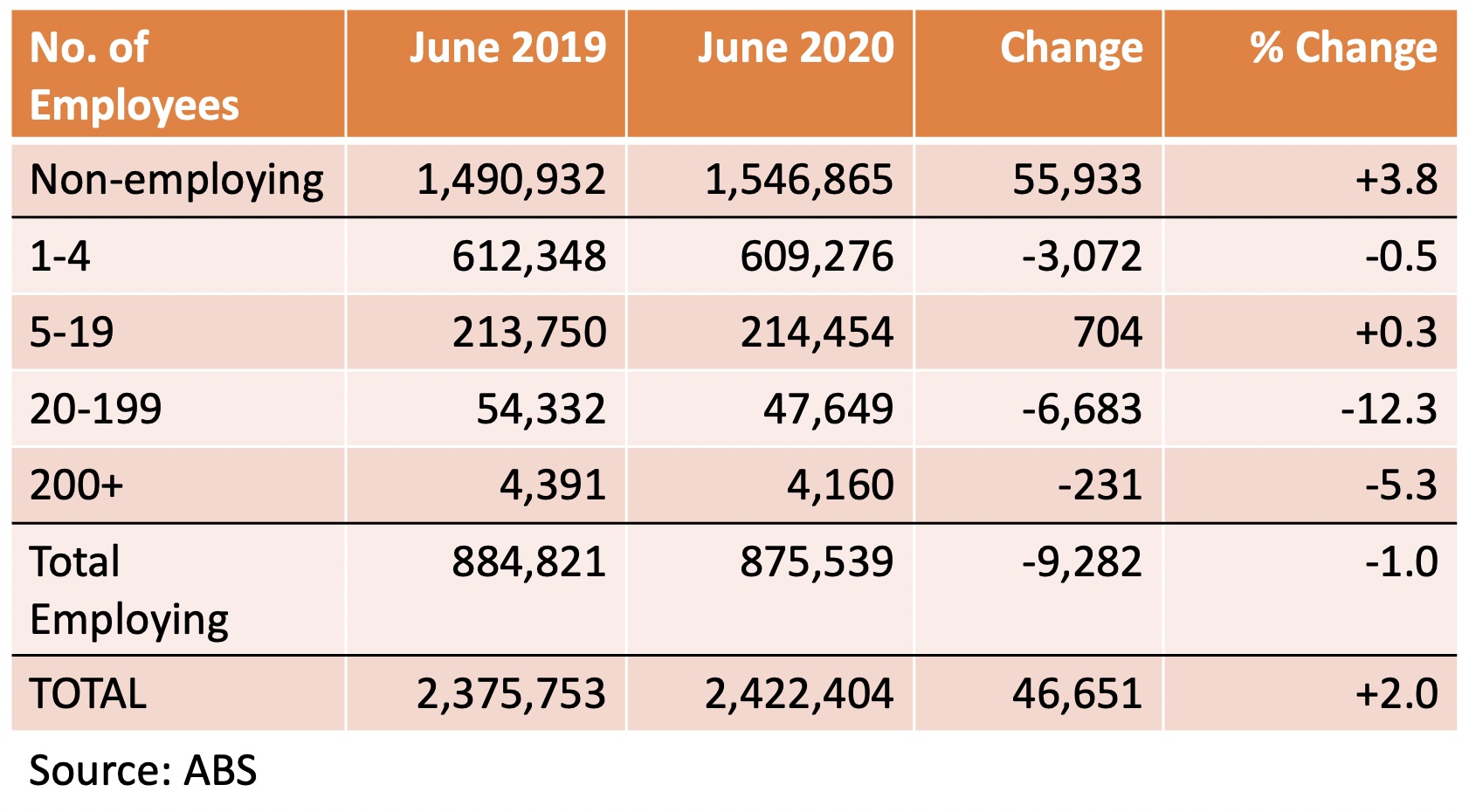

First, there are nearly 2.5m registered business entities, according to ABS data. Over 1.5m of these are designated as “Non-employing” – including sole traders, self-employed, independent contractors or freelances. Over 850 thousand establishments employ fewer than 200 people. Fewer than 5,000 businesses employ more than 200 people. Although there was an overall growth of 2% in the number of registered businesses, the largest increase was in the “sole trader” category, while the largest decreases were among medium-sized companies, and large enterprises. (See table below – the next ABS data is due in August.)

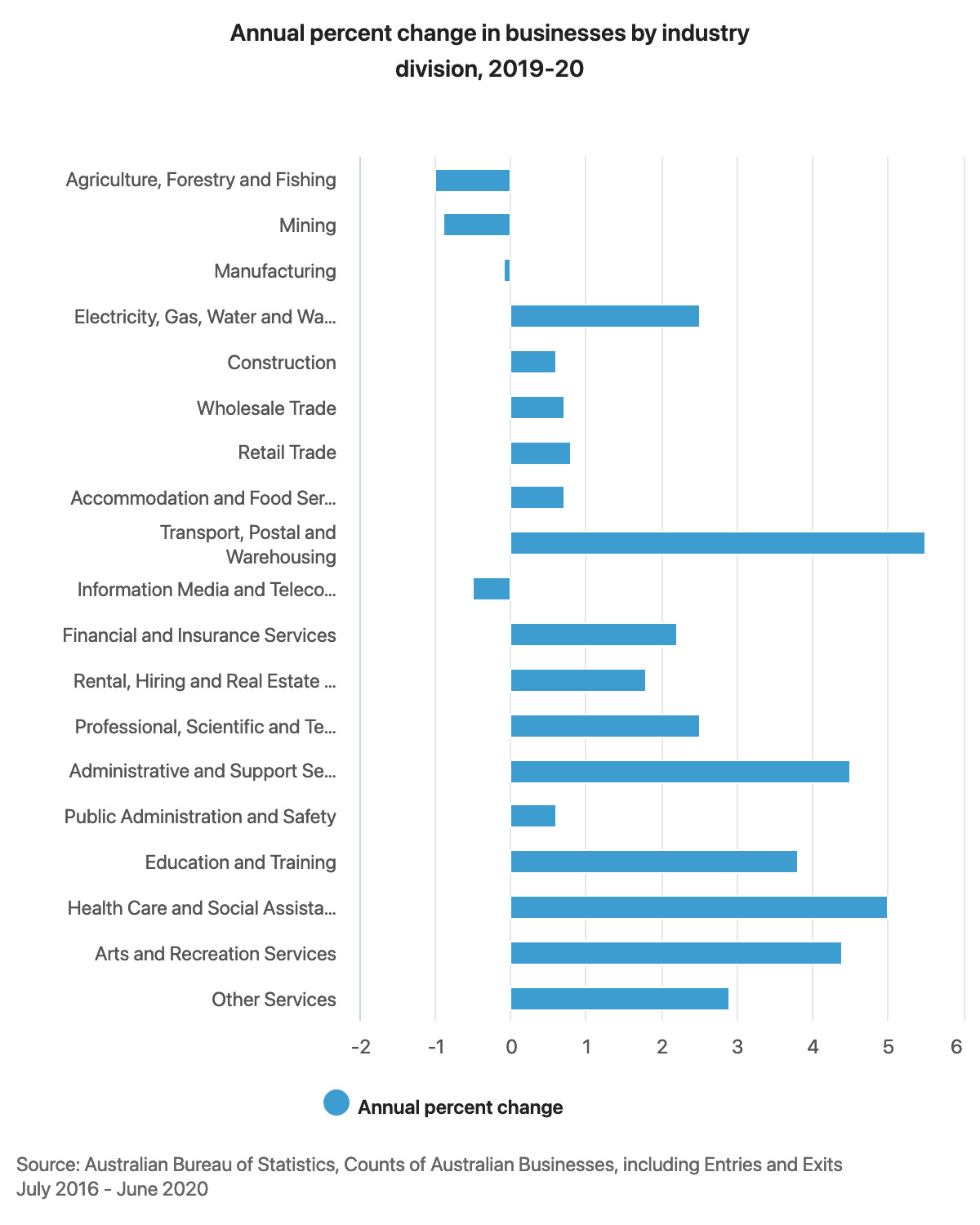

Second, the largest employment growth by industry sector in 2019-20 came from logistics and healthcare – no doubt in large part to the impact of COVID. Primary industries and mining both registered decreases.

Third, the main contributors to output (GDP) are Health and Education (13%), Mining (11%), Finance (9%), Construction (8%) and Manufacturing (6%) – based on a recent RBA Snapshot. But the data is always subject to further examination and clarification – for example, while construction employs over 1.1m people, many of these are engaged as independent tradies or through sub-contractors, and in spite of the huge number of major infrastructure projects (just look at Victoria’s Big Build and all the cranes in Melborne CBD), there was only negligible growth in overall employment within the sector. And while mining is a major contributor to GDP, it does not employ huge numbers of people (it’s actually on a par with the arts…), yet the fewer than 9,000 people who are employed as mining engineers are in the top 10 occupations by salary (according to ATO data analysed by the ABC.)

Some other factors to consider as we ask, “Where will wage growth come from?”:

- While most people are employed by SME’s, these companies are probably under the greatest strain when it comes to overheads and inputs, as they have relatively high fixed costs, and can ill-afford higher wages in the current trading conditions.

- On July 1, the Superannuation Guarantee is due to increase from 9.5% to 10% – some commentators suggest employers (especially SMEs) may have to reduce or offset wages to pay for the scheduled increase.

- We have an apparent choice between an asset-led recovery (inflated house prices – but risks leaving people “asset rich and cash poor” when interest rates go up ); a consumption-led recovery (reliant on higher wages so people feel comfortable to spend money); or an investment-led recovery (businesses need to invest in new equipment and projects to boost productivity, and not just bring forward planned expenditure thanks to tax incentives).

- The sectors where we need more people (health care, aged care, child care and education) are still among the lowest paid on a per capita basis.

- What is happening to boost manufacturing, or aren’t we interested in making things anymore?

- Our IT and technical skills shortages have been exacerbated by the absence of overseas students and graduates – there is anecdotal evidence of wage and hiring pressures in this sector, one which is probably more important to our future economy and sustainability than mining coal or building more roads.

- One leading economist reckons that household incomes have increased by 30% over the past 10 years. If wages have been stagnant, where has this growth come from? Is it because of tax cuts, low interest rates, quantitative easing, real estate prices (or their crypto holdings)? And do we actually feel any wealthier as a result?

Finally, will inflation and/or interest rates undermine any potential increase in wages?

Next week: Is Federation still working?