Last week, I achieved the eponymous age of The Beatles’ song, “When I’m Sixty-Four”, as featured on their “Sgt. Pepper’s Lonely Hearts Club Band” album. Like many of the people who commented on YouTube, I was just a kid when I heard this song on its release; and I, too, could not imagine being that age.

For one thing, at that time, back in the late 1960s, my grandparents, great uncles and great aunts were all in their mid- to late-sixties; to me they were already so old, even ancient. God forbid that I should end up like that! Of course, given their life experiences, perhaps it was not surprising that they seemed so wizened (physically and metaphorically) before their time. Living through two world wars and a deep economic depression takes its toll. Also, in 1967, life expectancy was around 72 years; now it’s close to 82. And back then, the UK state pension age was 65. Consequently, people seemed “old” because that’s how they were expected to behave, and they were treated as such by government and society alike.

Now I have reached this milestone myself, I realise more than ever before that aging is also a mental construct, not just a biological process. Hence the notion of “subjective age”. If you think you are too old to do something, then you are probably limiting your options (and narrowing your outlook). Little wonder that articles about “life begins at 60” seem popular!

I know have had a very different life experience to my grandparents. For example, two of them never went abroad, three of them never drove a car, and one didn’t live past the age of 50. Unlike them, I don’t have children or grand children, I have lived outside my country of birth for more than half my life, and I have traveled to far more countries than they ever did.

On the other hand, unlike many of my parents’ generation, many of whom enjoyed jobs with life-long career expectations, I have had a more erratic and inconsistent work experience – similar to my grandparents. In their cases, they either had to create their own work (e.g., small business owner) or endure periods of patchy employment. In my own case, I went into corporate employment at a relatively late age, and exited at age 50 – hitting something of a grey ceiling. Mainly for that reason, I have endeavoured to remain curious, stay open-minded, be flexible and willing to adapt – which I believe has helped me to maintain a “younger” subjective age. I think it also helps to have non-work pursuits and interests, so you can remain active if (and when) your employment comes to an end. Plus, having social interactions with people who are not all the same age as you can help to develop more of an inter-generational perspective.

One last comment – I was very surprised to read recently that according to a global study, boomers like me may be living longer, but not healthier, than our parents and grandparents. Despite medical advances, our lifestyles and other factors may result in more chronic disease and illness. I’m not suggesting that this decline is due to psychological ageing, but I can’t help thinking that if you say you are old, old age (and all its ailments) will soon catch up with you.

Recent media commentary suggests we have a housing crisis in Australia – ranging from affordability and supply, to quality and location, as reported here. Renters are being priced out of the market, ageing stock means houses that are too cold in winter or too hot in summer, and there aren’t enough homes to rent where people want to live. I suspect that all of these factors have been in place for several years, but the knock-on effects from the Covid pandemic have exacerbated these trends.

For background, I should explain that at the start of my career, I worked as a housing officer and paralegal in the UK. I worked for three different local councils in inner London, advising tenants, leaseholders and landlords on their respective rights and obligations – and where there were infringements, preparing prosecutions against landlords and their agents. I dealt with people facing harassment, unlawful eviction, homelessness and housing disrepair. Mostly, my work involved advising the parties of their legal position and available remedies, often I helped them reach an amicable solution, and occasionally I had to take enforcement action with the support of the council’s legal powers. The latter included injunctions against the threat of unlawful eviction, the issuance of proper rent records, repair notices, rehousing directives, and even compulsory purchase orders.

It was stressful, and at times confrontational, work – after 5 years, I was pretty burned out, and decided to make a career change. At the time, London (and the UK) was experiencing a huge amount of change that impacted both the public and private rental sectors. First, the Conservative government under Margaret Thatcher had introduced “right to buy” legislation, meaning public housing tenants could apply to buy the homes they lived in. Second, the government also introduced “mortgage interest relief at source” (MIRAS) which meant home buyers received tax relief on their interest payments. Third, central London in particular was going through a period of gentrification, with public money made available to property owners to improve and upgrade period homes. As a result, Georgian and Victorian houses that had been sub-divided into apartments (mainly occupied by long-term tenants) were restored to single family homes. Added to that, one of the council’s I worked for had been engaged in a “homes for votes” scandal, a “policy” to (re-)engineer the local demographics.

In the past, I’ve been both a tenant and a landlord, so I’ve also experienced some of these issues for myself. As a tenant, I’ve had landlords who denied that their properties were poorly wired or had defective plumbing (despite formal notifications from the council), and denied all requests to have the defects fixed. As a landlord, I’ve had tenants sub-letting to their “friends”, and who assured me that these “friends” could pay the rent.

So what is going on in parts of Australia, that there is such a misalignment between where tenants want to live, and vacant housing stock?

First, to touch on property ownership. Home owners don’t receive anything like the former MIRAS scheme in the UK, but there are various financial incentives for first-time buyers (such as zero stamp duty when buying a property off the plan), and during the Covid pandemic, some first-time buyers could access their superannuation (pension) fund to help with the deposit or down-payment. Property investors can take advantage of negative gearing to offset mortgage interest payments and costs of repairs against their income tax. These factors are generally considered to push up house prices – and despite recent interest rate rises, the cost of borrowing has remained at historic lows for more than a decade. Housing inflation means aspiring buyers are priced out of the market (especially as wages have not kept pace with inflation, let alone the rise in property prices). And landlords are now seeking to increase rents to offset rising interest rates.

Second, I’ve never really understood why some landlords don’t maintain their properties to an adequate standard – it surely detracts from the value of their assets, as well as deterring potential tenants. And when there may be improvement funds available (e.g., insulation grants, solar rebates) why wouldn’t they take advantage? On the reverse, should tenants have more powers to undertake essential repairs and improvements, and withhold rent to cover the costs? (Equally, I find it surprising that some tenants don’t feel it is their responsibility to undertake minor maintenance or running repairs, such as mowing the grass, clearing gutters or replacing cracked window panes.)

Third, it’s an economic imperative to have a supply of housing stock in the rental market. It helps people who prefer to rent rather then buy, it allows for workforce mobility, and it supports seasonal demand in industries like agriculture. I don’t believe that all rental stock should be held and managed in the public sector – it represents a huge obligation (not just an asset) on government balance sheets, tying up capital and incurring huge running costs. We need a component of public housing, but otherwise leave it to the private sector, with appropriate safeguards.

Fourth, why the apparent mismatch between supply and demand? On one level, developers are building the wrong types of properties and/or building in the wrong locations. Inner city areas have seen a massive growth in high-rise apartments over the past 20 years, supposedly in response to increased housing demand. In theory, these projects generate more yield for developers, although the apparent over-supply leads to depressed rents, and some banks won’t lend against these properties due to uncertain re-sale value and over-capitalised assets.

In the suburbs, archetypal quarter acre blocks have been sub-divided to cram in more town houses and units, or developers are building bigger houses (McMansions) on smaller plots, leaving minimal gardens and no breathing space between properties, as they build right up to the boundary lines. Many new suburban developments lack proper infrastructure and services (public transport, schools, shops, clinics), making them less attractive to renters – while the owners expect higher rents to cover the cost of their mortgages. Plus, many new properties have been built “on the cheap”, using inferior materials and design – hence the issues with heating/cooling. On the other hand, ageing stock, especially weatherboard and brick veneer structures, can also be hard to heat/cool. Many houses (new and old) lack double-glazing, for example, which would go a long way to resolving this energy conundrum.

Meanwhile, the recent lock downs in Melbourne (and to a lesser extent, Sydney) have meant many urbanites have moved to regional locations, putting upward pressure on property values and rents, pricing out locals who already live and work there. Of course, another reason for the mismatch in supply and demand is the growth in short-term lets, mainly for holiday-makers – such that local stock is taken out of the regular rental market. However, a lot of the Airbnb accommodation I have used over the years would never have been available on the rental market, because they were pre-existing holiday lets, or they are principal homes, where the owners are temporarily working abroad or interstate. And this type of flexible accommodation is also in demand by a mobile workforce that can, and prefers to, work from anywhere (so-called digital nomads).

None of which explains or resolves the current crisis. If governments want to address the bigger issues, they need to consider a range of solutions: updating building standards, upgrading land-use rezoning and planning regulations, encouraging a greater variety of housing development and management (soclal housing, shared ownership, property exchanges, rent holidays in return for repairs and improvements), and the use of modular/portable homes to meet fluctuating demand. All of which requires vision, and most party political objectives are driven by short term goals and the next election cycle.

* Apologies to Pere Ubu for (mis-)appropriating the title of their second album

A few weeks ago, two connected but unrelated news items caught my attention. The first concerned the death of an elderly man, who froze to death in plain sight on a busy city street. The second, published barely 10 days later, reported that the mummified body of an elderly woman was only found two years after she died. Much of the commentary surrounding both stories talked about public indifference (even callousness) and lack of concern for our neighbours, especially those who live alone.

I suspect that two years of pandemic, lock-downs and isolation have only amplified preexisting conditions. Depending on our perspective, we may choose not to do or say anything in these situations because: we don’t want to get involved, we don’t want to interfere, we don’t want to risk infection, we don’t feel adequately trained to deal with these situations, or we simply don’t have the time.

Scenarios like these can often make us think about how we might react in similar circumstances – the thing is, we won’t know until it happens. But equally, acquiring some basic skills or adopting some common protocols might help prevent future individual tragedies.

In my inner city suburb, during the pandemic, there has been a sense of “looking out” for your neighbours – some enterprising folk even organised local soup deliveries, and unwanted home produce was left by front gates. It was all totally spontaneous, but largely driven by existing relationships. If we want to do this properly, by fully respecting older neighbours’ independence whilst not interfering in their daily lives, we need some different community models.

One positive example came from the ABC’s inspirational documentary series, “Old People’s Home For 4 Year Olds”. Although a large part of the outcome was to help older people in building up their physical and cognitive skills, by also framing it about boosting pre-schoolers’ social development, it underlined the longer-term community benefits of such initiatives. It also showed that in raising mutual awareness of the need for social interaction, and by creating a level of co- and inter-dependency, communities can find practical solutions and achievable outcomes, often using existing and available resources more creatively.

How good is the Aussie economy? On the back of the stable outlook on our AAA sovereign credit rating,last week’s employment data showed a better-than-expected post-COVID recovery in terms of the headline unemployment rate and overall workforce participation. This has led to speculation of a potential uplift in wages, due to labour shortages amplified by the current halt on immigration (thanks to closed borders).

But where will this expected wage growth actually come from?

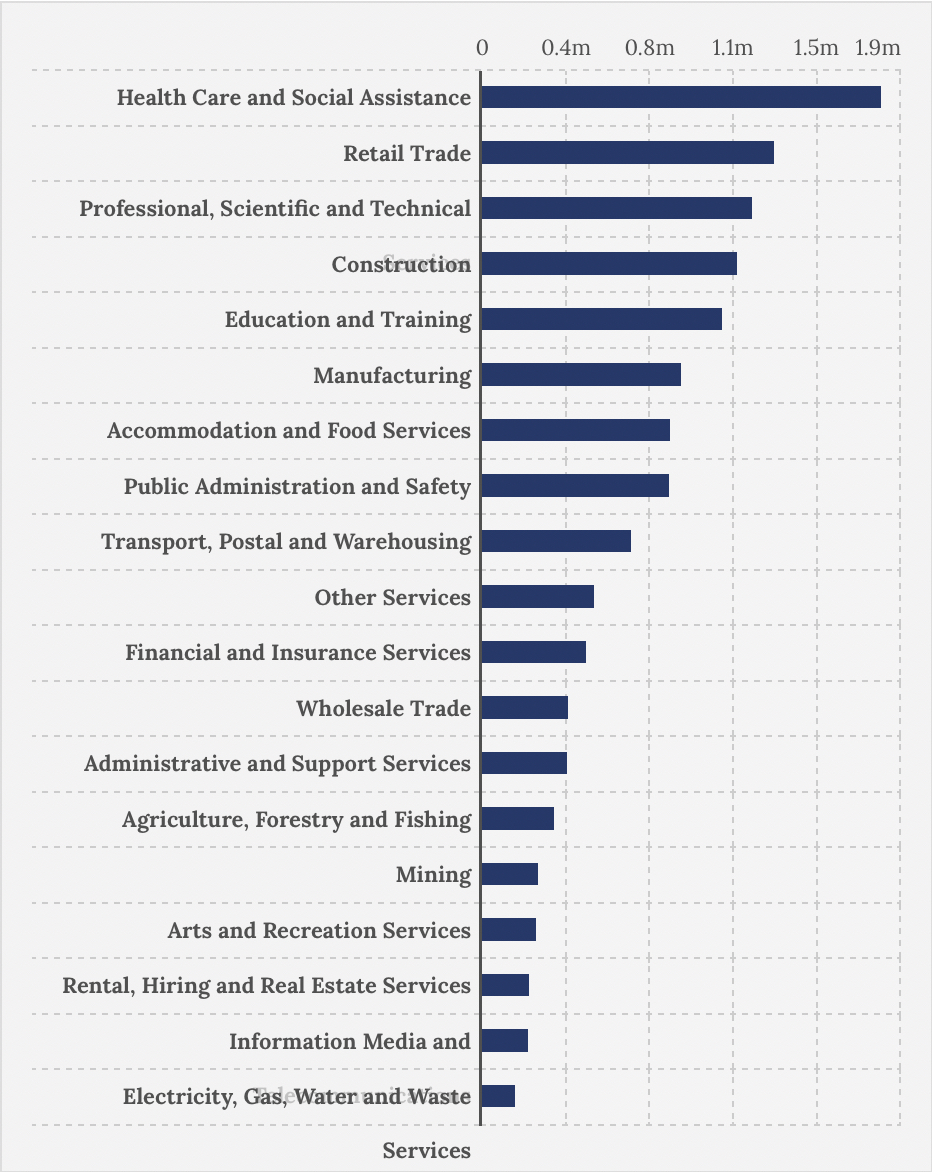

According to ABS data for February 2021, the top 5 industries by number of people employed are: Health Care; Retail Trade; Professional, Scientific and Technical; Construction; and Education. (See above chart.)

Now, contrast this with three other relevant data points: 1) the number of Australian companies by size; 2) the annual change in employment growth/reduction by industry; and 3) the national GDP contribution by industry.

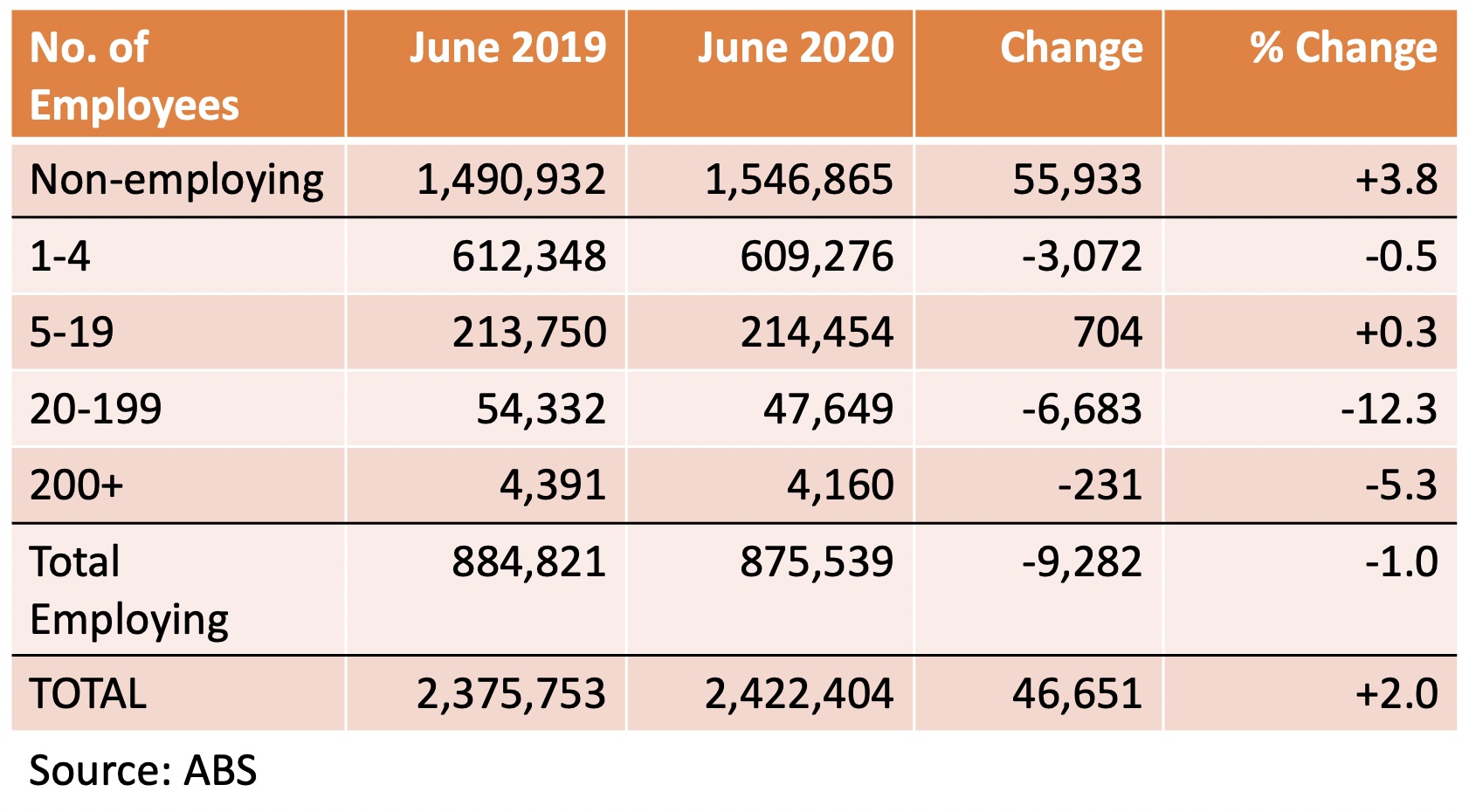

First, there are nearly 2.5m registered business entities, according to ABS data. Over 1.5m of these are designated as “Non-employing” – including sole traders, self-employed, independent contractors or freelances. Over 850 thousand establishments employ fewer than 200 people. Fewer than 5,000 businesses employ more than 200 people. Although there was an overall growth of 2% in the number of registered businesses, the largest increase was in the “sole trader” category, while the largest decreases were among medium-sized companies, and large enterprises. (See table below – the next ABS data is due in August.)

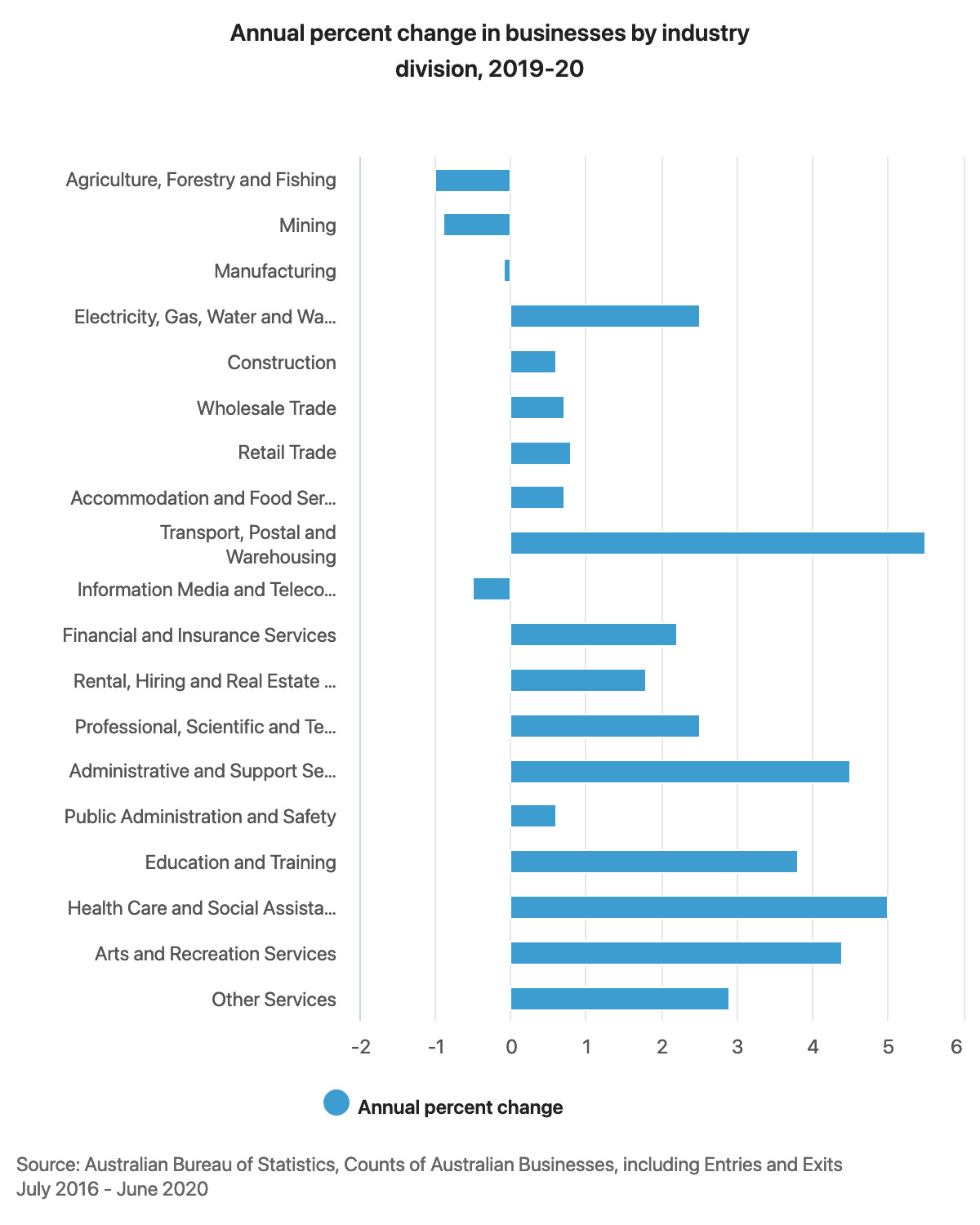

Second, the largest employment growth by industry sector in 2019-20 came from logistics and healthcare – no doubt in large part to the impact of COVID. Primary industries and mining both registered decreases.

Third, the main contributors to output (GDP) are Health and Education (13%), Mining (11%), Finance (9%), Construction (8%) and Manufacturing (6%) – based on a recent RBA Snapshot. But the data is always subject to further examination and clarification – for example, while construction employs over 1.1m people, many of these are engaged as independent tradies or through sub-contractors, and in spite of the huge number of major infrastructure projects (just look at Victoria’s Big Build and all the cranes in Melborne CBD), there was only negligible growth in overall employment within the sector. And while mining is a major contributor to GDP, it does not employ huge numbers of people (it’s actually on a par with the arts…), yet the fewer than 9,000 people who are employed as mining engineers are in the top 10 occupations by salary (according to ATO data analysed by the ABC.)

Some other factors to consider as we ask, “Where will wage growth come from?”:

While most people are employed by SME’s, these companies are probably under the greatest strain when it comes to overheads and inputs, as they have relatively high fixed costs, and can ill-afford higher wages in the current trading conditions.

On July 1, the Superannuation Guarantee is due to increase from 9.5% to 10% – some commentators suggest employers (especially SMEs) may have to reduce or offset wages to pay for the scheduled increase.

We have an apparent choice between an asset-led recovery (inflated house prices – but risks leaving people “asset rich and cash poor” when interest rates go up ); a consumption-led recovery (reliant on higher wages so people feel comfortable to spend money); or an investment-led recovery (businesses need to invest in new equipment and projects to boost productivity, and not just bring forward planned expenditure thanks to tax incentives).

The sectors where we need more people (health care, aged care, child care and education) are still among the lowest paid on a per capita basis.

What is happening to boost manufacturing, or aren’t we interested in making things anymore?

Our IT and technical skills shortages have been exacerbated by the absence of overseas students and graduates – there is anecdotal evidence of wage and hiring pressures in this sector, one which is probably more important to our future economy and sustainability than mining coal or building more roads.

One leading economist reckons that household incomes have increased by 30% over the past 10 years. If wages have been stagnant, where has this growth come from? Is it because of tax cuts, low interest rates, quantitative easing, real estate prices (or their crypto holdings)? And do we actually feel any wealthier as a result?

Finally, will inflation and/or interest rates undermine any potential increase in wages?