No sooner had Netflix launched in Australia than Treasurer Joe Hockey announced the imposition of GST on “intangibles” purchased from overseas vendors. The Treasurer has also indicated that the GST-free threshold for on-line imports will be lowered from the current $1,000. Dubbed the “Netflix tax”, Australian consumers should now expect to pay more for their digital content such as video, music, software and e-books, even though on most evidence, we are already charged more for comparable products than in other markets.

Geo-blocking is already an obstacle for Australian consumers…

Backdrop

We all know why the Treasurer has proposed this scheme: the Government has to make up for declining tax receipts, and appease the States who are squabbling over the allocation of GST revenue between them. Plus the current Senate inquiry into corporate tax avoidance by companies like Apple, Google and Microsoft (who divert locally sourced income to offshore entities to reduce their income tax liability in Australia) is driving the public and political agenda on global tax minimization schemes (which are nothing new, of course).*

But it’s not as simple as slapping an extra 10% on the price of a movie download, even though GST is a relatively easy and cost-effective way of generating tax revenue. For one thing, there is little consistency in how vendors currently sell their digital products in Australia. Secondly, geo-blocking is already an obstacle for Australian consumers, leading to the sort of content piracy infringement that will now make local ISP’s and their subscribers more vulnerable to legal action, following the recent “Dallas Buyers Club” court ruling. Thirdly, local retailers who have long campaigned to have the GST-free threshold removed or lowered fail to acknowledge why customers prefer to shop from overseas vendors.

Goods & Services Tax

GST (similar to VAT in Europe) is a simple consumption tax. It applies to the sale or supply of most items (except things like fresh food and health services) at a flat rate of 10%.

Even better, the Government and the tax authorities rely on businesses to collect, report and remit GST receipts, making it relatively cheap to administer (when compared to other taxes) via the Business Activity Statement process managed by the Australian Taxation Office.

The GST is a key topic of the current review of the tax system – likely to result in a higher rate (or different rates), and/or broader application to items not currently included.

Vendor Inconsistency

In principle, I don’t have a problem in paying GST on digital items I buy from overseas vendors – but there is so much inconsistency that there is a risk of consumers having to pay two lots of sales tax.

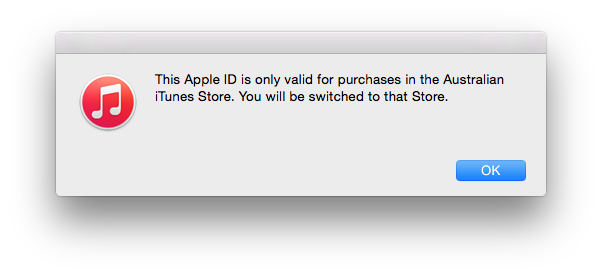

For example, every iTunes receipt issued by Apple Pty Ltd (an Australian entity) states that the sale amount already includes GST – in which case, Apple should be remitting that component to the ATO, and no need for a price increase.

However, Adobe chooses to invoice me from Ireland, and as such no GST (or VAT) is applied, but I am charged forex fees, even though the invoice amount is expressed in Australian dollars, because my bank treats this as a foreign transaction.

Meanwhile, although some UK vendors I buy from direct do not apply GST/VAT on my orders (Amazon UK included), others do – meaning I risk having to pay both the GST and VAT. As a further sign of vendor inconsistency, Amazon’s US store does not appear to deduct US sales tax for foreign customers; neither the UK or US Amazon stores sell music downloads to Australian customers; and Amazon’s Australian store only sells e-books and apps.

Geo-blocking

The decision in the “Dallas Buyers Club” IP infringement case brought by Voltage Films, has again drawn attention to Australia’s poor reputation for copyright piracy as evidenced by the number and frequency of illegal downloads.

Some journalists have commented that distributors often delay the local release of imported content (for various reasons) although this was not seen as a justification for piracy (and quite rightly so).

While foreign films are frequently released later in Australia, it’s interesting that TV (even free to air channels) has woken up to this, and now broadcasters rush to fast-track imported shows to keep audiences happy.

It’s also interesting to note that the Productivity Commission, as part of its competition policy review of IP laws, has suggested that if local rights holders and distributors choose not to exercise their commercial rights, under a “use it or lose it” model, third-party distributors would be able to step in. This also has the potential to undermine the archaic industry practice of geo-blocking, whereby sales of music, film and TV content (physical and digital) are restricted by territory.

Local retailers and distributors need to lift their game

Does the absence of GST really encourage consumers to buy from offshore retailers? I would beg to differ.

Local rights holders often do not bother to make content and products available in Australia. And local retailers won’t usually stock products if they are not readily available from wholesalers or distributors.

I recently had to contact an overseas artist, the UK record label and its Australian distributor several times to make their music available online in Australia. The local distributor had not bothered to release the content, even though they had the rights, but geo-blocking prevented me from accessing it legally from overseas suppliers.

It’s the combination of inadequate local distribution, non-availability, higher prices and lacklustre service that encourages Australian consumers to buy from overseas, even if that means circumventing geo-blocking. In many cases, I doubt the addition of GST will be a serious deterrent to online overseas shopping.

In my own case, I once found that the local branches of a global retail brand chose not to stock the item I wanted, and their US parent geo-blocked me from ordering on-line. So I resorted to buying in the “grey” or parallel imports market, from an offshore vendor willing to ship direct to Australia. It was still cheaper, even after shipping costs, and even if GST had been added (I probably paid US sales tax on the transaction anyway), than if I had bought from a local retailer (assuming they bothered to stock the item).

Hopefully, this debate on GST and the Productivity Commission’s review of competition policy will finally give local retailers an incentive to do a better job of serving their customers.

* The debate on corporate tax minimization might want to look at where “value” is created, and where the revenue is booked, that gives rise to a tax on the resulting profits. For me, the retail value of intangibles such as digital products is created when someone pays to download them, at the point of sale – i.e., in the consumer’s geographic location. Although the vendor may argue that the IP is owned by an offshore entity to whom they must pay royalties, the individual download itself does not have any standalone value, until it is accessed by the consumer. Even a high rate of royalty repatriation could not be more than the retail price, so logic might suggest that local profits should be taxed accordingly.

Next week: What can we learn from the music industry?