Last week’s Jobs and Skills Summit hosted by the Federal Government in Canberra was clearly designed to be a statement of intent by Prime Minister Anthony Albanese and his Labor administration. Part policy endorsement, part policy road map, the Summit was hailed (by the Prime Minister at least) for reaching agreement on “36 immediate initiatives”. By all accounts, it was a jolly affair and everyone in the Government sounded very pleased with themselves. The reality is that despite some significant pronouncements, most of them lack detail, many of them relate to existing initiatives, a number of the “36 agreements” were largely concluded and/or telegraphed ahead of the Summit – and of course, the one item that got most attention was the most divisive: the renewed prospect of multi-employer collective bargaining.

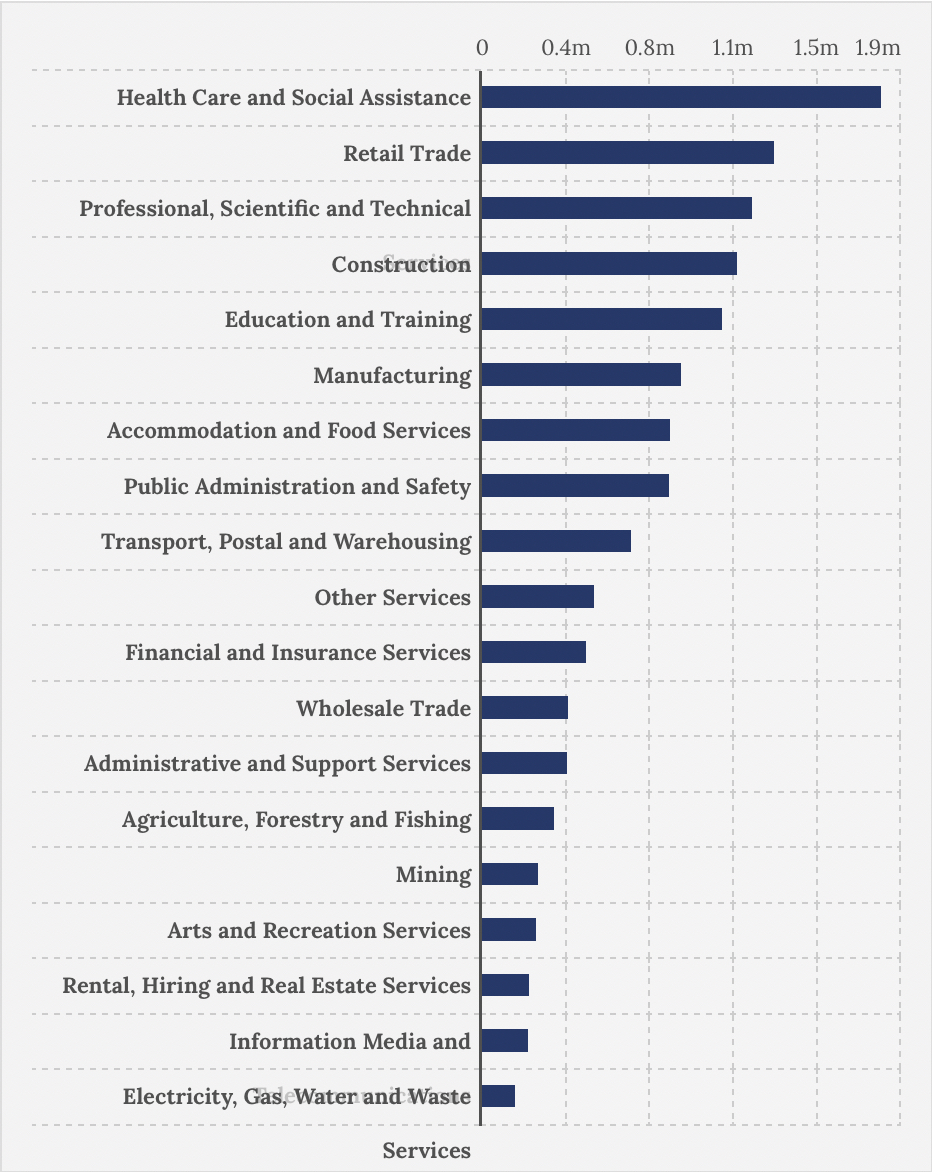

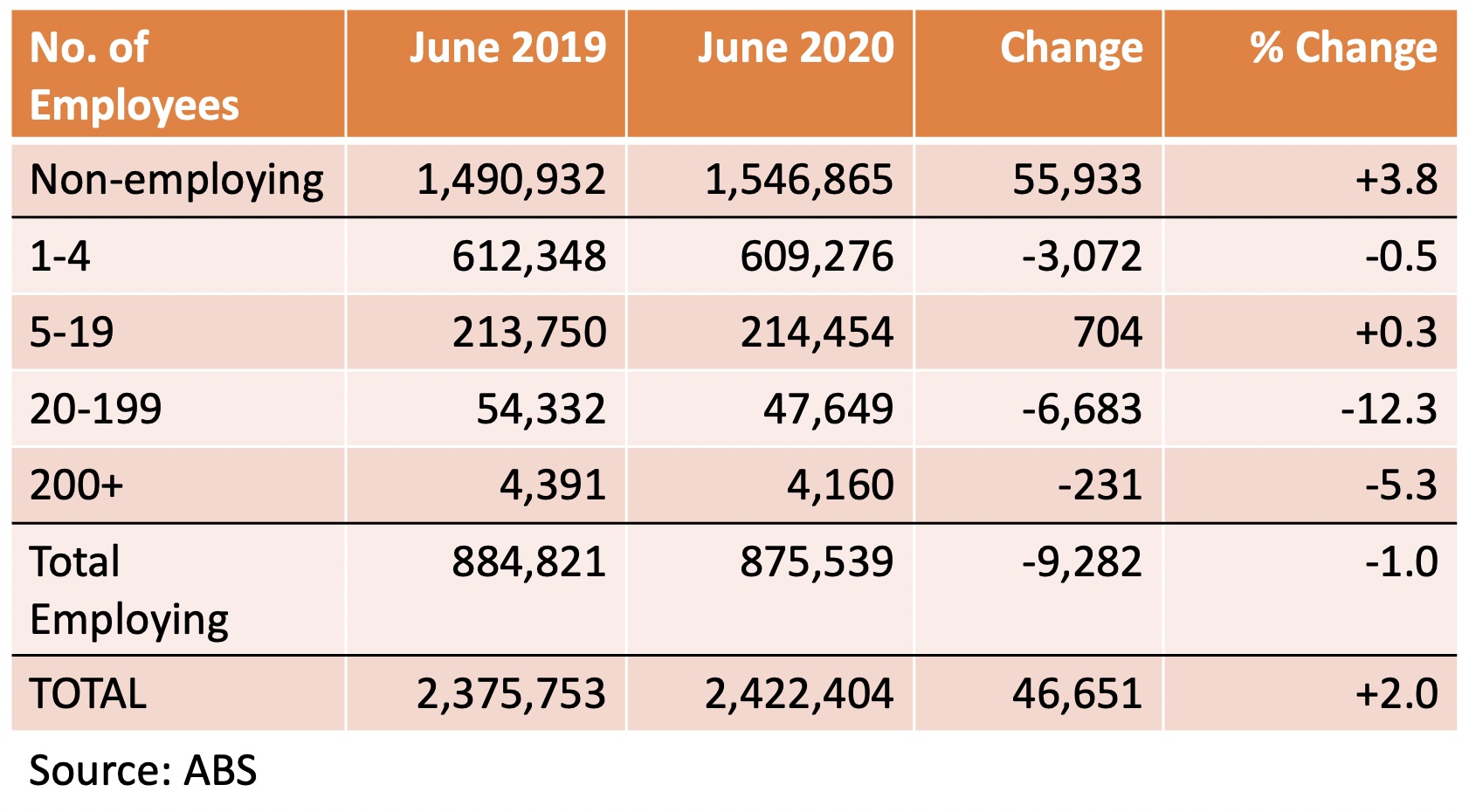

Number of Australian companies by employment size, 2018-2022 (Source: ABS)

Number of Australian companies by employment size, 2018-2022 (Source: ABS)There were some contentious views about the small business association’s pre-Summit MoU with the ACTU. Some peak industry bodies and other commentators felt that COSBOA had “sold out” in apparently agreeing to sector-wide negotiations on pay and conditions. However, this does not appear to be the case – COSBOA is merely seeking better co-operation and consultation on areas of mutual interest, and is not endorsing any form of enforced unionisation or compulsory sector bargaining. There have been suggestions that sector-wide collective bargaining will result in higher wages, but without more detail, and pending greater clarity on the “Better Off Overall Test”, this will simply add friction to the current debate about wage and employment growth.

If we do return to a previous form of Industrial Relations policy, it’s interesting to look at the latest ABS data on Australian businesses by employment size (table above). I think it’s worth noting the number of working people in Australia who are employed by SMEs. Large employers are actually small in number, so if multi-employer collective bargaining does come into effect, it could mean tens of thousands of businesses will be involved, and many probably for the first time. On the other hand, in an industry like construction, which is both highly unionised and covered by significant industry awards, many workers are either self-employed or they are employed by independent sub-contractors.

Representation at the summit was reasonably well-balanced, between Unions (including Industry Superfunds), Business (individual companies and industry associations), the NFP and Community sectors, Academia, Think Tanks, and of course Politics. The absence of the Leader of the Federal Opposition meant that his voter base was effectively disenfranchised, although his Deputy (and Leader of the National Party) did attend. Go figure.

Much was said about “streamlining” and “updating” parts of the Industrial Relations regime. Like Australia’s tax laws, the system of Modern Awards as overseen by the Fair Work Commission feels unwieldy, unnecessarily complex, over-bureaucratic, at times vague, and often archaic bordering on arcane. There are currently over 140 different awards in place – some of them relate to an individual company, some to a particular trade or profession, and some cover a whole industry. Interpretation is often in the eye of the beholder as to whether or not it applies to a particular employer and/or employee – here is an extract from one award:

“NOTE: Where there is no classification for a particular employee in this award it is possible that the employer and that employee are covered by an industry modern award or a modern award with occupational coverage.” (Emphasis added.)

I should add that one reason given by the Labor Government for removing the prohibition on sector-wide collective bargaining is because the process for employers to request an exemption from the relevant Minister is “too cumbersome”. I don’t see how this is so given that much of the IR system is overly bureaucratic. Surely the reason for this administrative process is to avoid collusion and other cartel-like activities that would otherwise fall foul of competition law and anti-trust provisions.

The Summit had some notable things to say about gender equality and pay parity, (“Legislate same job, same pay”), training, immigration and child care; but some proposals sound vague without defined objectives (“Boost quantum technology research and education”); draconian if they inhibit workplace flexibility, especially in seasonal industries (“Limit the use of fixed-term contracts”); or too aspirational without more detail such as specific goals and measurable targets (“Leverage greater private capital into national priority areas, including housing and clean energy”). We know that Labor ministers have been vocal in their dislike of the so-called “gig economy” (a “cancer” on the economy, and “I’d like to regulate the sh*t out of it”), but perhaps they need to do more to understand why some workers actually prefer it, and what benefits it brings in terms of workplace flexibility, especially in start-ups and emerging sectors, many of which are SMEs from where much of our longer-term innovation and employment opportunities actually come.

One item that didn’t receive as much attention was the “Digital Apprenticeships Scheme”, which (subject to details…) would likely have the combined support of the Tech Council of Australia and the ACTU. Certainly, despite a vibrant and innovative IT sector, and some notable high-tech and high-end manufacturing businesses in Australia, we lag behind in STEM education, and lack basic digital literacy skills in the wider population. (Hence the need for adjustments to the skilled migration scheme?) A friend of mine who runs a small manufacturing business in Melbourne recently hired an Office Assistant. The successful candidate claimed to be proficient in standard productivity tools such as Word and Excel. In fact, they didn’t know how to COPY-PASTE, nor how to use the SUM-ALL function, which are both very basic routines. They thought they could “wing it” by watching a YouTube video…

Finally, if there is one note of caution or concern about the Summit, it is the niggling thought that this was more of a talk-fest, and that any new ideas to have emerged were either covered by existing programmes and “policy settings”, or were already in train. Going through the list of Outcomes, I counted at least three dozen separate initiatives (Plans, Schemes, Agreements, Reports, Statements, Codes, Programs, Compacts, Task Forces, Working Groups or Funds) many of which already exist, or were part of Labor’s election promises, or have been proposed prior to the Summit. (And that list excludes Federal Ministries and Government Departments.) Sounds a lot like “Talks about Talks”, with “new” money already allocated and spoken for (hence Labor’s push back on some of the implied costs of the Summit proposals). At worst, this “wish list” represents a huge amount of expensive and bureaucratic overlay, whereas we need agile and flexible economic, education and employment measures.

Next week: Finding a Voice