Last Monday, May 11, at around 19:23 UTC, the third Bitcoin halving occurred. This event is currently scheduled to happen approximately every four years, and is a core mechanism in Bitcoin’s protocol. In short, combined with the finite supply of bitcoin (BTC), the halving acts as an anti-inflationary measure by reducing the number of BTC payable to the miners who confirm each block of transactions, and maintain the integrity of the blockchain ledger. By using dedicated, high-powered computers to solve Bitcoin’s complex algorithms, the miners earn BTC as rewards for their efforts (and to help recoup their energy costs). As a result, the halving is an integral component in measuring key metrics in BTC’s performance, including pricing, supply and mining profitability. What happened around the time of the halving provides for some interesting analysis before and after the event.

BTC price dropped dramatically just prior to the latest halving event – the above graph is plotted using the hourly closing value of Brave New Coin’s Bitcoin Liquid Index.

The halving is programmed to occur after every 210,000 blocks, which themselves are “mined” approximately every 10 minutes. Last week’s third halving was triggered when block number 629,999 was confirmed – from block 630,000 onward, the block reward reduced from 12.5 BTC to 6.25 BTC per block, and is designed to continue halving until the block reward reaches 1 Satoshi (0.00000001 BTC).

Usually, financial markets have already priced in events such as the halving, so traders don’t expect the event itself to have an immediate impact on price. (Think of the halving as just one type of “corporate action” that is peculiar to cryptocurrencies and digital assets. Others might include hard forks, coin burns, and token lock ups.) As with company results and profit announcements, traders and analysts are usually prepared for the best (or worst).

However, leading up to the latest halving, BTC briefly touched a 3-month high of US$10k, before going through an almost typical “market correction” of a 20% decline immediately prior to the halving event. BTC has since recovered some of those losses, and in any case, the price performance before and after each halving event has become yet another indicator of long-term price movement, as the following chart illustrates:

Source: Brave New Coin

Other metrics to watch include: “hash rate” (the degree of difficulty, and therefore the amount of computing power, to solve the algorithms and mine each block); transaction fees (if miners can’t earn as much from mining activity, they are expected to start increasing their network fees); the price of electricity (as an input cost to mining); and even the cost of computing power itself (as older machines become less efficient and therefore less profitable, while newer, more powerful and more expensive processors come to market).

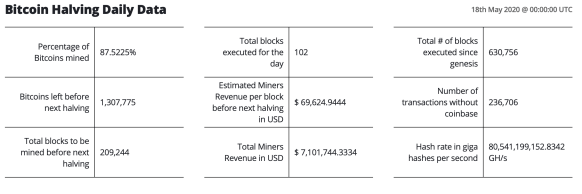

Indeed, different scenarios used to predict the exact date of the next halving are largely based on the hash rate, which has been relatively volatile before and since the halving, and transaction fees likewise escalated (and then settled down again) around the time of the halving. Key data to track as part of halving analysis and forecasting can be seen in the table below from Brave New Coin:

Source: Brave New Coin

Other interesting developments around the time of this latest halving include a legendary hedge fund manager reported to be buying BTC as a hedge against inflation; an increase in open interest on CME’s BTC futures contracts (assumed to be coming from institutional clients); and an intriguing message attached to block 629,999 (“NYTimes 09/Apr/2020 With $2.3T Injection, Fed’s Plan Far Exceeds 2008 Rescue”). Given the recent quantitative easing measures pursued by many governments and central banks in response to the Covid-19 pandemic, this choice of headline echoed the message attached to the genesis or very first Bitcoin block, mined in 2009, soon after the GFC (“The Times 03/Jan/2009 Chancellor on brink of second bailout for banks”).

Finally, as more data and analysis attaches to the halving events, they form the basis of a fundamental aspect of understanding how financial instruments perform over time – giving rise to the BTC equivalent of a 1, 5 or 10 year yield curve, which in turn will create more sophisticated derivatives and hedging tools, and another level of comfort for traditional and institutional investors.

(My thanks to friends and colleagues at Brave New Coin and Apollo Capital.)

Next week: “How do I become a business strategist?”