I spent the past week in Tokyo on behalf of Brave New Coin, meeting with various participants in the cryptocurrency industry – from exchanges to brokers, from industry bodies to information vendors, from connectivity providers to technology platforms. Given its share of Bitcoin trading volumes, and the legal developments currently in motion, Japan is now the focus of attention as it navigates towards a fully regulated and orderly cryptocurrency market.

Bitcoin is now accepted in Bic Camera stores in Japan (Photo: Rory Manchee – all rights reserved)

On my previous visit to Japan, I commented on the extent to which it was still a cash economy – even major museums and galleries don’t accept plastic, and my pre-paid foreign currency card issued by a major Australian bank was only accepted at a limited number of ATMs: 7-Eleven, and Japan Post. But according to expats I spoke to last week, this situation has changed over the past couple of years.

One of the reasons I was given as to why Japan is taking a lead in regulating cryptocurrencies is its previous perception of having a somewhat lax approach to money laundering. Part of this might be explained by the limited technical integration and interoperability with the global banking system (somewhat akin to Japan’s approach to telecoms, where in the past, it was impossible for overseas visitors to use their mobile phones on the domestic network).

In addition, as China has cracked down on most things crypto, so has Bitcoin trading activity shifted to Japan. This growth in Bitcoin trading volumes can also be linked to Japan’s passion for retail forex trading, now expanding into crypto.

Earlier this year, the Japanese government passed legislation that recognises bitcoin as a legal form of payment. (Note: this does not mean that bitcoin is legal tender – shops do not have to accept it; but if they choose to take it as payment for goods and services, then it is no different to paying in cash or by credit card when it comes to things like consumer rights, for example.)

Later this month, the main regulator, the FSA is expected to announce new regulations to govern cryptocurrency exchanges and brokers. Currently, exchanges that accept Yen deposits for cash trading of crypto must be licensed as payment institutions. By the end of March 2018, my understanding is that all exchanges and brokers must be fully licensed to operate – for both cash trading, and futures and margin trading. Anywhere between 20 and 50 exchanges have applied for a license.

Currently, participants in the “legacy” securities and futures industry are either registered with the JSDA or the FFA. Likewise, it is expected that the FSA will appoint a similar self-regulating entity to have official oversight of the cryptocurrency markets, under the overarching authority of the FSA. However, there are two rival blockchain and cryptocurrency industry associations that are vying for this role – which is where things become a little political. One group claims to represent the “pure” crypto world, whereas the other might be seen to represent more of the traditional market. No doubt the FSA would prefer not to have to choose…

Key considerations for the FSA are retail investor protection, and market stability. The total market cap of all cryptocurrencies is now around US$150bn. If we assume that 10% of these assets are held in Japan, when compared to the total capitalisation of the cryptocurrency exchanges themselves, this creates a significant risk for the FSA should there be a market collapse or a run on Yen-based crypto deposits.

Equally, the FSA does not want to stifle innovation in an area of financial services where Japan is keen to take the lead. For example, Japan has witnessed a couple of bitcoin-denominated corporate bonds (more like privately syndicated short-term commercial paper) that demonstrate an investor appetite for this new asset class.

Meanwhile, in preparation for this new regulatory environment, and in anticipation of the increased interest by major banks and asset managers, there is a project underway to create an institutional-strength order management platform connecting banks, brokers and exchanges. I also heard of offshore fund managers looking to launch a crypto-based ETF for distribution in Japan.

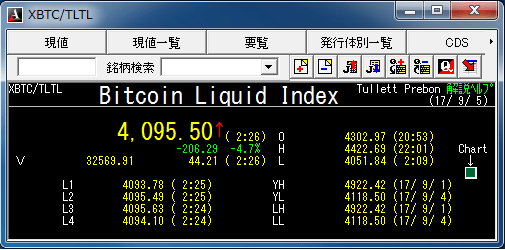

Finally, at the risk of blowing our own trumpet, Japan’s leading financial vendor, Quick is now quoting the Bitcoin Liquid Index (BLX) alongside other FX data it distributes from around the world:

NOTE: The comments above are made in a purely personal capacity, and do not purport to represent the views of Brave New Coin, its clients or any other organisations I work with. These comments are intended as opinion only and should not be construed as financial advice.

Next week: Tech, Travel and Tourism

Apart from Bitcoin’s latest all-time highs (and of course, CryptoKitties), the main topics on Blockchain solutions, cryptocurrency trading, token issuance programs and digital asset management were:

Apart from Bitcoin’s latest all-time highs (and of course, CryptoKitties), the main topics on Blockchain solutions, cryptocurrency trading, token issuance programs and digital asset management were: